Get your FREE 30-day trial.

Please complete all fields.

Blockchain is a technology that promises to fundamentally change how we share information, buy and sell things, and verify the authenticity of information we rely on every single day — from what we eat to who we say we are. And because it can facilitate all of this in secure, efficient, and transparent ways across many different domains, the effects can be transformative — every business, government, and individual can benefit.

“Blockchain can drive profound change across a range of industries and sectors, reimagining the way we do so many things”

Such is blockchain’s promise that Gartner predicts it will result in $176 billion in added business value by 2025, and $3.1 trillion by 2030. Yet blockchain is also a complex technology, and many companies are finding it challenging to unlock its full value, given complexities around networks, data models, partner adoption and skills gaps amongst their employees.

So how can it achieve this promise, exactly? What is blockchain technology, for a start, and how should organizations separate the reality from the hype?

For many people, blockchain is a complex topic and not the easiest concept to grasp. Here's a preview of some of the questions this article will answer:

What is blockchain technology?

How does blockchain work?

What are the benefits of blockchain?

How can businesses use blockchain?

How will blockchain disrupt industries, from financial services to healthcare?

What is blockchain technology?

Simply put, blockchain technology is a new secure architecture that saves and traces data in a way that is distributed and verified by a network of computers.

“By using a blockchain...as a kind of connective tissue between different decentralized data stores, things can get really interesting”

Common features include:

Records stored in a digital ledger. Blockchain can be used to record and encrypt any type of transaction involving an exchange, such as the transfer of funds or the ownership of property.

A distributed ledger that maintains a transaction list. The list of transactions is replicated across a number of computers in almost real time, rather than being stored on a central server.

A peer-to-peer network that maintains the transaction records. The ledger’s only accessible to a network of partners, who share the work of updating and maintaining it.

No intermediaries in the peer-to-peer network. There is no one point of control or central authority, and no third-party mediators (lawyers or banks, for example) are involved.

Verification via cryptography and digital signatures. Cryptography and digital signatures are used to prove participants’ identity and authenticate transactions.

Public and private networks

Companies or individuals can decide to share a ledger across a public network or a private one. Public networks — as the name implies — are open to all. Here, millions of people may participate at any one point in time. These “public ledgers” operate without the need for identity information, and most users adopt pseudonyms.

Bitcoin was the first public blockchain network, and it remains one of the largest. Another example is Ethereum, a platform that can host transactions involving smart contracts.

Businesses can also choose to set up a private network, where existing users invite others to transact and interact. In this case, the ledger’s transactions aren’t visible to the public and the very existence of the network itself may be hidden.

Verification by consensus

With both types of network, any changes to the ledger must take place through consensus — that is, records can only be altered if a majority of the ecosystem agrees that a change should be made.

Usually, networks agree upfront on a definition of what this means in practice. With bitcoin, for example, participants must follow a detailed set of rules that set out exactly what constitutes a “valid” transaction or block.

With most blockchain ecosystems, certain mechanisms are put in place to make it extremely hard for individual bad actors to tamper with the records.

“When dealing with suppliers or counterparties or clients, it can be transformative to know that paperwork, products, payments — even people — are all as they should be.”

Let’s take the example of how a bank transfer might work on a blockchain database. When Simon transfers funds to Sue, all the people in the network — rather than a single authority, such as a bank — must verify that this transfer (or transaction) actually took place. Because all transactions are transparent across the network, providing everyone in the chain with a clear view of where the data originated, it’s relatively easy for participants to spot if anyone tries to delay, reverse, or otherwise break the verification rules.

At the same time, should a miscreant try to add a false “block” to the chain of records, they would typically need to gain access to and control more than 50% of the computers being used across the network in order to do so — something that would be almost impossible to achieve.

In short, Simon’s network is not vulnerable to a single point of failure. In this way, blockchain can enable stakeholders to confidently and securely share access to data and information.

Blockchain solutions use many different kinds of consensus protocol. One common approach is a “Proof of Work” algorithm, where network participants must solve a challenging mathematical puzzle before they can verify transactions. In return, they are given rewards and incentives so they will stay involved. In public networks such as Bitcoin, these rewards come in the form of cryptocurrencies or tokens.

Blockchain in action

Let’s take a look at some other examples of how blockchain works in practice. A leading healthcare provider currently relies on electronic medical records to provide hospitals and doctors with pertinent health information about new and existing patients. However, those records are often incomplete or missing information. With blockchain, doctors, hospitals, insurance providers, patients, and more can come together to view and update medical histories in a unified ledger. Blockchain makes it easy for healthcare professionals to view and update those records, and for patients to get a comprehensive view of their entire medical history — resulting in a trusted, simpler, and faster process for any patient who wants to transfer between institutions.

“We’re going to see a lot more of this type of cross-cutting action across industries, where companies rally round blockchain technology to create a common data model that can deliver more value to the customer”

Or take the example of how a supply chain might benefit from blockchain technology. Businesses adopting this type of solution can set up a trusted network with the partners they transact with, based on a platform that allows all stakeholders to access and manage any previously-siloed data. All transactions are transparent on such a network, and the traceability of products and goods is readily available. Stakeholders can apply actionable processes to this data and relay any pertinent information about products and goods to their customers (that is, the consumer).

This approach can help companies monitor costs, labor efficiency, and even waste and emissions at every point of the supply chain. That has big implications for enterprises seeking to reduce inefficiencies and add traceability and security into the way they manage complex supply chains. Continuous, near-real-time access to a chain of events taking place can help organizations reroute shipments on the fly, for example, and better coordinate shared manufacturing facilities, equipment, and infrastructure to optimize supply chain capacity.

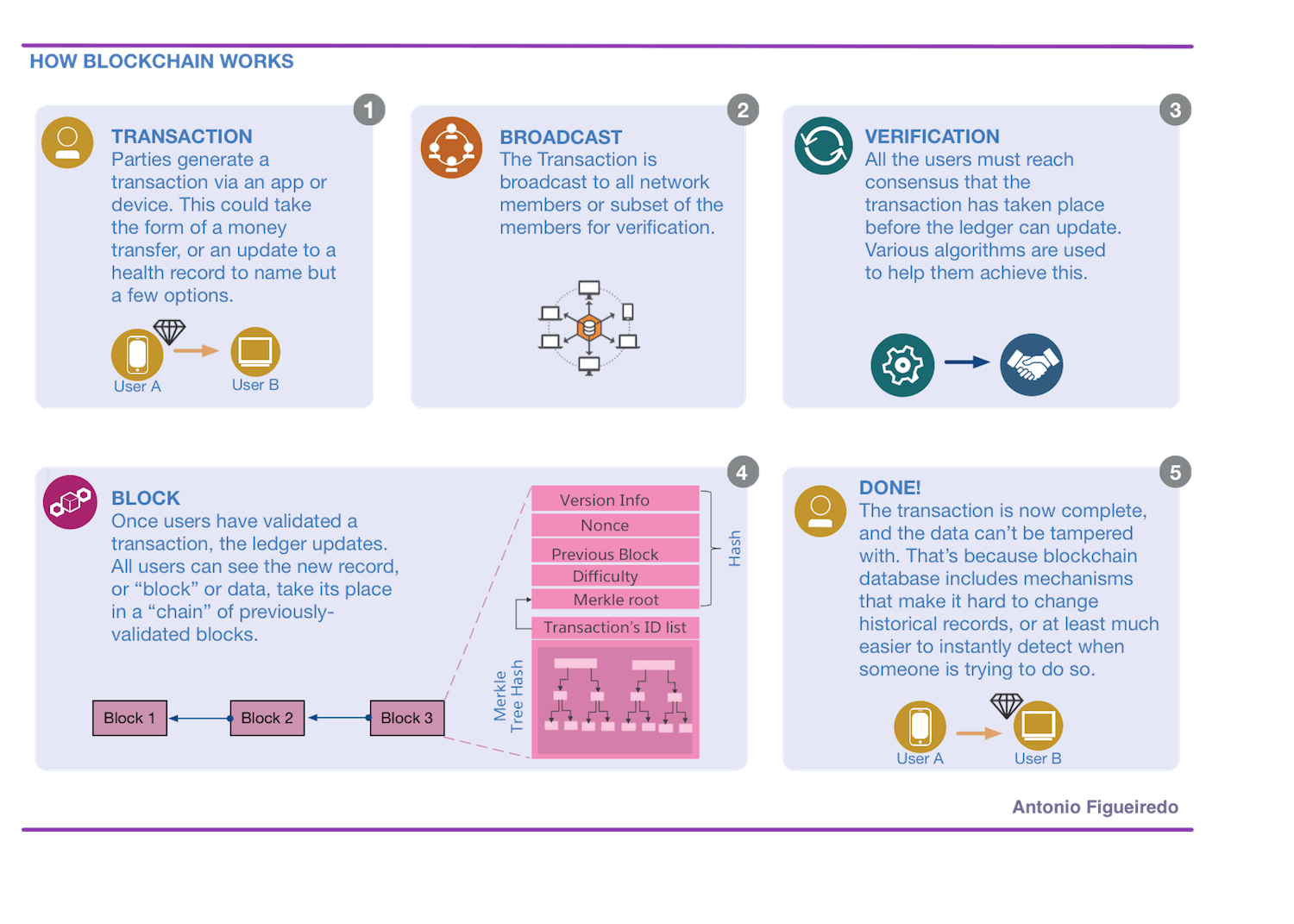

How does blockchain work?

The diagram below gives more detail on how transactions are recorded and validated in a blockchain database.

What are the benefits of blockchain?

To help answer this question, let’s take the example of Company ABC, which — like many legacy business networks — stores its data in multiple places and formats. It’s also vital to the company that the integrity of its transactions with its external partners can easily be validated.

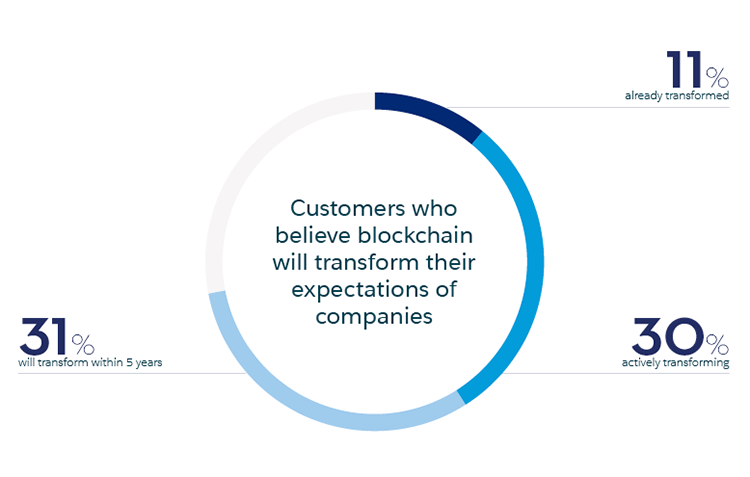

“72% of customers (both consumers and business buyers) believe that blockchain technology will transform their expectations of companies within the next five years.”

Because the company’s databases are siloed, CIO Joe Black found problems with data reliability and accuracy, with out-of-date or duplicated records, lost data, and administrative errors. These inefficiencies add costs through fees and delays. The situation also creates friction for teams across the business through redundant and onerous paperwork. At the same time, reconciling ABC’s data with the records held by the company’s external partners has been a lengthy, challenging process. Joe’s worried the situation may even open up opportunities for fraud and crime.

To address these issues, Joe decides to move the company onto a blockchain-based database or shared ledger. This brings together all the relevant data from the company’s parallel systems and databases, along with its partners’ data. Now, one integrated, interoperable source of truth is available for all parties involved (including any external partners). The difference is remarkable — now, every stakeholder across the business has instant access to all the data and information that pertains to any specific business process.

Other benefits Joe and his colleagues start to see include:

More robust security. Because data is secured using cutting-edge approaches such as cryptographic keys, blockchain networks are more resilient to data tampering and cyber attacks.

Faster, cheaper transactions. Blockchain databases do not need traditional third parties such as banks and lawyers to authenticate transactions — that role is filled by the technology. By eliminating the need for intermediaries, businesses can streamline their processes and reduce costs.

Greater transparency and traceability. Because every network member in a blockchain database has access to the entire database of transactions and their history, they benefit from real-time transaction-level assurance. Such systems can also be much easier to audit.

“The more data lakes, or silos, we create, the more technical risk we create,” says Amber Baldet, CEO and co-founder of decentralized application development startup Clovyr. “So, an ability to unbundle data is really relevant across every industry at this point.”

“One integrated, interoperable source of truth is available for all parties involved (including any external partners). The difference is remarkable — now, every stakeholder across the business has instant access to all the data and information pertaining to any specific business process.”

“Also, by using a blockchain or distributed ledger as a kind of connective tissue between different decentralized data stores, things can get really interesting. Maybe it’s decentralized document signing within your organization, or across your own sub-legal entities. The point is that there are so many things you can then do without needing to get together 20 different banks, say, around a table with a bunch of lawyers before deciding that you can start a development process.”

Scott Likens, New Services and Emerging Technology Leader at PwC, believes that blockchain is set to be a foundational technology for maintaining trust in the digital era. As he points out: “When dealing with suppliers or counterparties or clients, it can be transformative to know that paperwork, products, payments — even people — are all as they should be. You can then do more with partners and customers and automate more of your transactions with them.”

How can businesses use blockchain?

There are many indications that blockchain will significantly affect the business landscape. Here are a few current use cases:

Blockchain for CRM

Combining blockchain technology with customer relationship management (CRM) systems offers businesses a way to significantly enhance existing workflows, and build trusted partner networks that extend CRM. Blockchain can help to extend trust, transparency, and traceability in every customer interaction, as well as break down business boundaries and data silos.

Let’s take a closer look at how blockchain technology can help a CRM system achieve such things. Companies benefit from the following:

A more efficient way to gain a 360-degree view of the customer. Because blockchain is based on a distributed network architecture, data silos break down. Rather than multiple copies of a customer’s details ending up duplicated across numerous systems, all applications have access to just one set of records. As a result, companies can reduce redundancy and increase responsiveness. Also, CRM-based platforms can aggregate more contextual and detailed information about participants and its products and feed the blockchain business network with richer information.

Enhanced security. On a blockchain, each piece of code is protected with powerful cryptographic tools, which enhances security. In addition, data records are irreversible. No transactions can be erased, so data can’t be tampered with.

Richer insights. As the quality of data insights into customer activities typically improves with scale, blockchain’s decentralized network approach can provide whole ecosystems of businesses in a blockchain network with deep insights into their customers’ preferences and expectations, in near real time.

Data quality and accuracy. Data integrity is critical in any ecosystem where system updates are prone to human error or negligence. Combined with other technologies such as the Internet of Things, a blockchain-based CRM solution can help businesses glean more actionable insights from their data, without the need for human intervention.

Blockchain for customer experience

Research shows 72% of customers (both consumers and business buyers) believe blockchain technology will transform their expectations of companies within the next five years.

It will do this by:

Providing a secure environment. As blockchain increases security in business–customer interactions, companies gain new trust. For consumers, the authenticity and safety of goods in a supply chain can be verified. As they transact and share data, they can also be more confident their data won’t be misused or compromised by malware, viruses, and breaches.

Making transactions in near real time. Blockchain can enable a transaction to be recorded and accessed by multiple parties in near real time — thus transforming customer service speeds.

Delivering more customized experiences. “Since blockchain enables consumers to selectively and securely share their data, they’ll likely feel more confident in doing so — enabling companies to customize products and services,” says Likens.

Blockchain can also help companies earn loyalty in other ways. Consider how a customer loyalty program can run on a blockchain network: because the technology can connect different loyalty program schemes and make the points they distribute interoperable, customers can conveniently store all of their collected points in one digital wallet, and use it to make transactions — a frictionless process that encourages engagement.

“Of course, it’s not just B2C that will be affected. I believe blockchain’s also poised to revolutionize B2B, in particular, creating trusted networks and processes between businesses so the partner ecosystems can be activated in a wholly optimized and automated way,” says Joshua Q. Israel Satten, Blockchain Partner at Wipro Limited.

Blockchain for productivity

Adopting blockchain solutions can help companies ensure their workforces become more productive over time. The reason lies with the technology’s power to create systems that are more reliable and accurate, reducing the occurrence of out-of-date or duplicated records, lost data, and potentially costly administrative errors.

A shared ledger approach can be especially effective when it’s used in conjunction with smart contracts. Already deployed by companies across the financial services sector, supply chains, and the legal profession, these software programs can be layered over the infrastructure of a shared ledger to automate and simplify business processes and arrangements. Terms execute automatically when predefined triggers occur, without relying on expensive third parties to enforce the bargain.

“Blockchain can have tremendous benefits for the employee experience”

For example, a firm can create invoices that get paid automatically once a truck delivers a product to a distribution center or share certificates that send stockholders dividends once profits reach a certain level.

And since smart contracts on blockchain can automate mechanical tasks (confirming data, enforcing contracts, processing payments, and more), employees can free up time for more interesting work.

“Blockchain can have tremendous benefits for the employee experience,” says Satten. “If an organization’s enterprise architecture harnesses DLT and smart contracts, and makes use of customized web-based applications alongside customized UIs, it can massively cut down on the overall number of systems used. At the same time, it can automate processes, better secure its information, and reduce errors. That means employees get an improved user interface with more digitization and operations interoperability, which can significantly impact productivity.”

Blockchain for fundraising

Blockchain technology — in the form of initial coin offerings (ICOs) — can facilitate fundraising for companies as an alternative to the traditional debt or capital funding mechanisms offered by banks, venture capital firms, and private equity firms.

Such an approach is based on tokenization. Here, digital tokens created on a blockchain network are used as an alternative way to denominate value — acting as a substitute for money, for instance.

Because such tokens can be used to represent any kind of tangible asset, they can be applied to a very wide range of business processes. In the real estate sector, innovative use cases include tracking and trading tokenized pieces of a property. Here, the tokens can allow for “fractional ownership,” or the ability for a qualified real estate owner to split up their property and sell off equity stakes.

In the case of ICOs, a company sells a predefined number of digital tokens to the public. Some startups have raised substantial sums by creating and then selling their own digital tokens — technology company EOS, for example, raised $4.2 billion in 2017.

How will blockchain disrupt industries?

Some of the most-cited use cases for blockchain involve the following sectors:

Financial services. Many startups eager to disrupt traditional players deploy blockchain to develop applications that aim, for example, to cut out the number of intermediaries involved in existing transaction processes, such as stock exchanges, cross-border payment networks, and money transfer services.

“Their goal is to reduce complexity and cost. There’s also a major focus on developing blockchain solutions to counter fraud and ensure the integrity of data,” Sandra Ro, CEO of the Global Blockchain Business Council says. “Obviously, all of this has been a big wake-up call for banks and other financial institutions. As they try to understand these developments and their potential impact, we’re seeing them invest in blockchain. They’re setting up internal teams, investing in startups, and creating common initiatives to understand the potential and search for use cases that can be implemented with minimal risk.”

Healthcare. Healthcare startups are exploring ways to use blockchain to streamline the sharing of medical records in a secure way, protect sensitive data from hackers, and give patients more access to — and therefore control over — their information.

Organizations have also been seeking to develop blockchain-based healthcare applications that can deliver such things as anonymized data pools for research companies, and new ways to fight counterfeit drugs.

Food. Some organizations are exploring blockchain-based solutions that bring industries together using entirely new business models. IBM, for example, has set up a blockchain-based food safety initiative with Walmart that brings together growers, processors, distributors, and retailers.

By creating a permanent, shared record of food-system data, the companies involved hope it will be much easier and quicker to trace produce from farm to store. In this way, any investigations into contaminated food can be significantly sped up, while Walmart and its partners also have more efficient ways to authenticate the origin of food and provide insights about the conditions and pathways through which the food traveled. Such an ecosystem of transparency and accountability can help build consumer trust.

“We’re going to see a lot more of this type of cross-cutting action across industries, where companies rally round blockchain technology to create a common data model that can deliver more value to the customer,” says Andrew Conn, Director of Product Design, Emerging Technology at Salesforce. “I believe we’ll get to a place in the near future where we’ll have many different industry coalitions or ‘partner ecosystems’ of this type competing against each other, each with the customer at the center.”

When is blockchain a good fit for your business?

One of the challenges for blockchain’s proponents is that its emergence has been accompanied by levels of hype that, as many commentators point out, aren’t warranted. It’s certainly true the technology is not the solution for every business problem. It's also a complex technology that warrants considerable initial research and thought on how exactly to integrate it into existing processes and technology stacks.

Companies looking to mine its considerable strengths should first ensure they understand the business issue they want to address, and how the technology can help.

“Companies do need to understand very precisely what problem they are looking to solve and whether blockchain is in fact the correct vehicle to get it done.”

Here are six questions to determine whether blockchain may be a good fit for your business:

Do you want to solve a business problem, rather than an integration problem? Blockchain is at times mistakenly positioned as an integration technology, but that’s not a core strength. If integration’s your goal, you may be better off using an API, Enterprise Service Bus (ESB), or web service.

Does your business process require inherent irreversibility? This quality is foundational to blockchain, so ask yourself whether it would help you achieve your business objective or hinder it.

Do you want to transfer objects of value from one party or entity to another? If this is the case, consider whether what you intend to do will benefit from immutability. Also, does it require consensus? If the answer is “yes,” you might benefit from using blockchain.

Do you want to transfer information across organizational boundaries? If your use case involves some level of managing cross-organizational trust, deploying blockchain can help. It can also be useful if you want to simplify the process between you and upstream or downstream business partners.

Do you want to target an ecosystem, rather than a few parties? Consider whether the problem you want to solve requires (significantly) more than two participants. If it is just a handful, integration might be the way to go. If you are targeting an ecosystem, blockchain may be the right choice.

Do you have a clear strategy for engaging and driving adoption with partners? Without their adoption of blockchain, the positive impact to your business will be limited.

Research shows more than one-fifth (22%) of IT leaders have already identified a use case for blockchain within their organizations. And those who have mapped blockchain’s capabilities to their businesses aren’t wasting any time; the same amount of IT leaders (22%) are actively working on a blockchain project.

“Blockchain can drive profound change across a range of industries and sectors, reimagining the way we do so many things,” says Ro. “Right now, for example, the technology is poised to disrupt how we manage health records, fight voter fraud, and distribute welfare, to name just a few areas. The possibilities are endless.”

Learn more about Blockchain by taking our new Trail — Blockchain Basics — over at Trailhead!