Get your FREE 30-day trial.

Please complete all fields.

Elevated consumer expectations and the rise of online marketplaces haven’t reduced the need for consumer goods (CG) companies to work with retailers. Today, fast-moving consumer goods annually earn $1.01 trillion in the U.S. — and 95% of those sales come from traditional retail.

At the same time, it’s no secret that traditional retail is a challenging environment, in light of recent store closures and Amazon changing the game.

Given this retail landscape, Salesforce researchers conducted a global survey of 500 CG leaders to discover how retailer challenges are impacting their businesses. We compiled our findings in Consumer Goods and the Battle for B2B and B2C Relationships. Here’s a preview of key findings from the report. We’ve also included insights from Sunil Rao, global head for consumer goods go-to-market at Salesforce, on what these findings mean for CG leaders.

1. Poor retail execution leads to lost merchandising spend

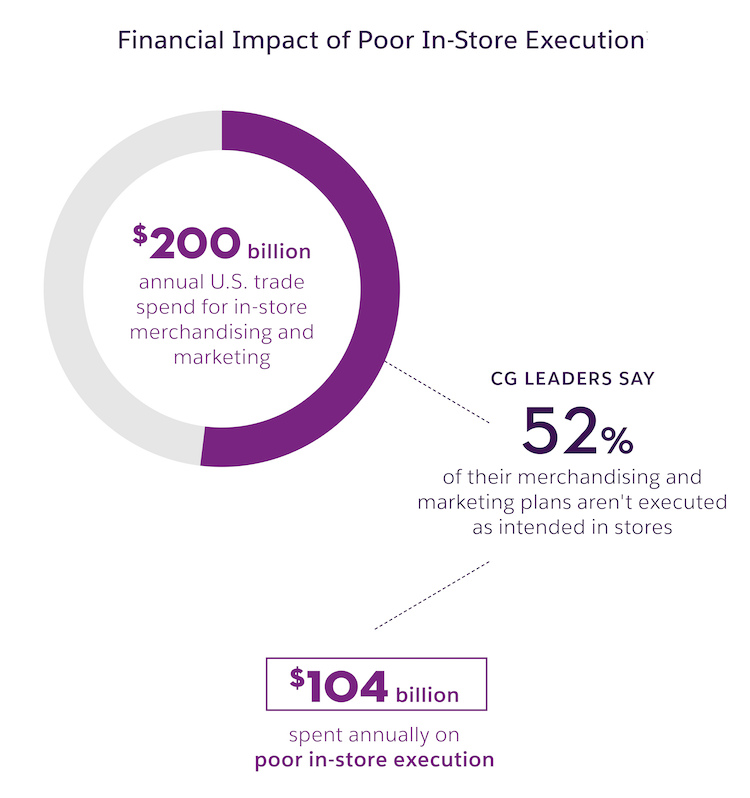

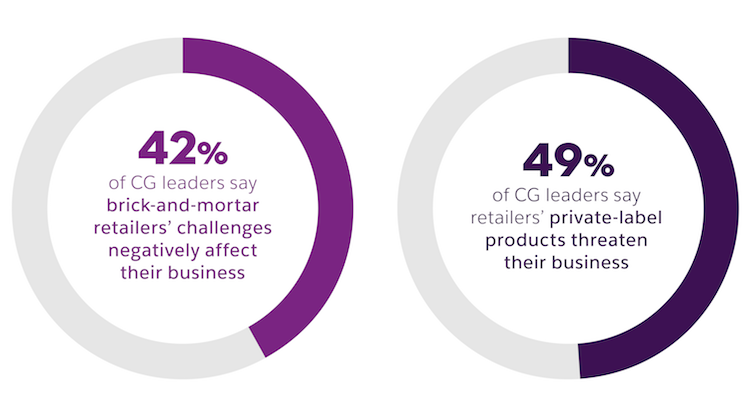

Forty-two percent of CG leaders say that the challenges retailers face — such as store closings and margin pressure — also negatively affect their business. In this climate, CG leaders face challenges in growing the trillions of dollars in their brick-and-mortar supply chain. When asked what percentage of their merchandising and marketing plans are executed as intended in brick-and-mortar stores, CG leaders said only 48% hit the mark. At the same time, CG leaders in the U.S. spend $200 billion annually on trade spend for merchandising and marketing.

That means CG companies are spending $104 billion in the U.S. alone on poor in-store execution.

According to Sunil, “The retailer relationship is still key. In this ongoing battle for consumer mind share, retailers and brands need to play together to survive. Improving in-store execution still remains a powerful lever–carving our cost from the bottom line while supporting top-line growth through an elevated consumer experience.”

2. Private-label brands are a business threat

CG leaders are keeping an eye on retailers’ burgeoning private-label lines that compete against their own products. In fact, 49% perceive retailers’ private-label products as a business threat.

Indeed, powerful private-label brands from the likes of Tesco, Hema, Costco, Amazon, and Walmart are soaring to new heights. In 2018, Costco’s Kirkland brand earned nearly $40 billion — an 11% increase from 2017 (and more sales than Campbell Soup, Kellogg’s, and Hershey combined).

Sunil says that although private-label brands bite at their heels, CG companies still can win at retail locations: “It’s more important than ever for CG leaders to tell a compelling story to consumers. By focusing on consumer experience, personalization, and impeccable service, CG leaders can ensure relevance, no matter what other brands populate the shelf.”

3. Barriers to data access are high

In an industry where access to consumer data is integral to accelerating innovation and time to market, less than half (43%) of CG leaders are completely satisfied with their ability to leverage customer insights from traditional retailers.

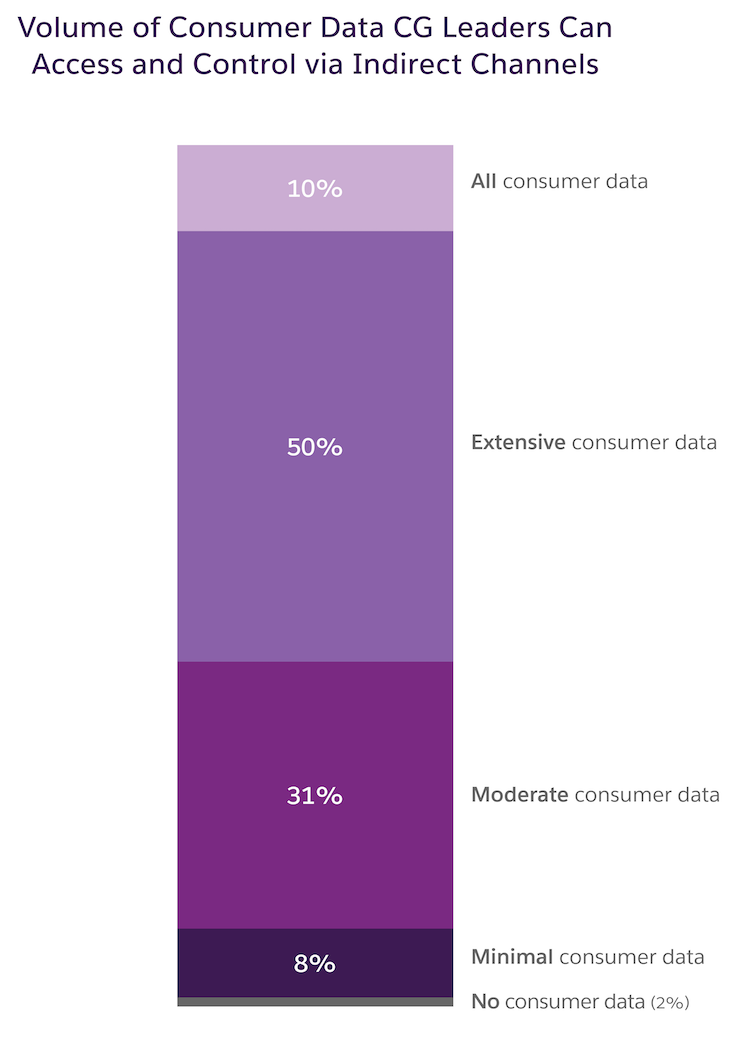

Marketplaces and wholesale channels also sit on volumes of data that CG leaders need, but 41% of them can only access a moderate amount or less of data from these combined sources.

The good news? CG leaders are working to fix this. Sunil notes, “Data is the bedrock of AI, enabling real-time personalization and automation at CG companies. Accordingly, CG leaders are prioritizing data accessibility – for example, our study found that 82% plan to increase investments in first-party consumer data access in the next three years.”

Where there are challenges, there’s room for improvement. CG leaders have major opportunities to improve in-store assortment, data access, and retailer relationships. For more insight into the priorities and challenges of 500 global industry leaders, download the new report: Consumer Goods and the Battle for B2B and B2C Relationships.