Get your FREE 30-day trial.

Please complete all fields.

The rippling effects of COVID-19 on the economy has overwhelmed everyone. With the unemployment rate at 13.3%, people are trying to save their homes, their businesses, and support their families. Banks are flooded with customer requests to help delay debt payments or alternative financing options. Your employees want to help alleviate customer stress, but are navigating new government programs, adjusting to work from home, and now are having virtual empathetic conversations. As a banking leader, you are faced with balancing how to help customers immediately, educating your employees remotely, and understanding the long-term credit implications of your actions.

This is an opportunity for banks to reestablish relationships with families and businesses as a trusted advisor. Influential leaders in financial services around the globe know they must be part of this recovery. This means leading with empathy, understanding pain points, and ways you can help. The financial services industry is in a better place than it was during the 2008 Economic Recession and is poised to become a foundation for stability and support.

Here we discuss ways you can deliver an empathetic trusted experience that can identify, engage, resolve, and lead customers to financial recovery.

Your customers’ financial stability is changing daily, increasing the demand for new credit and financial solutions. You must identify your at-risk customers to proactively provide solutions to alleviate financial pressures. This can be a challenge as most banks lack visibility and connection into both credit portfolios and customer analytics to manage risks across all product lines and departments. By creating a single source of truth with your data, you can have visibility into your operations and customer financial wellness.

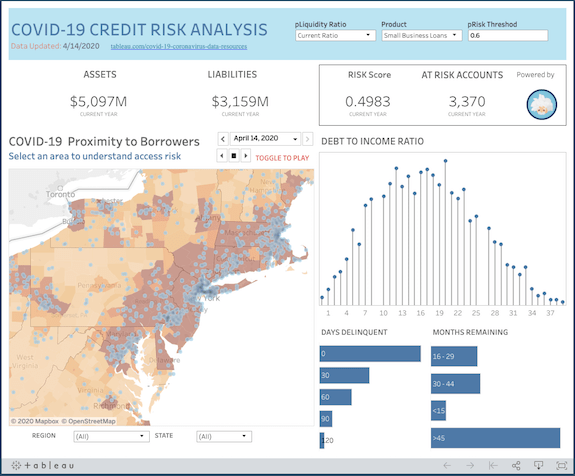

Start with connecting your platform and banking systems to your back, middle, and front departments through integrations with APIs or Mulesoft. Mascoma Bank leveraged Mulesoft to connect to their core banking system. This allows you to capture financial account data, service inquiries, and virtual meetings from any channel in one place. Now you have created a single source of truth. Analytics tools like Tableau and Einstein Analytics for banking can reveal real-time business insights to quickly sense and respond. Below is an example of a Credit Risk analysis of Small Business Loans in proximity to COVID-19 cases. Employees can see which small business customers might be affected by COVID-19 closures and proactively reach out to help.

By better understanding your customers, you can identify who needs immediate help and predict what areas could be impacted in the future. Use these insights as guidelines to adjust your operating model, protect the bank from the negative impacts of credit defaults, and revenue compressions. Now is the time to listen and focus on creating programs your customers need.

Once your data is providing valuable insights, it’s time to make it actionable. Banks have had to make quick decisions in response to new economic programs and customer requests. How do you know which operations to alter to meet the new requirements and make it all digitally accessible?

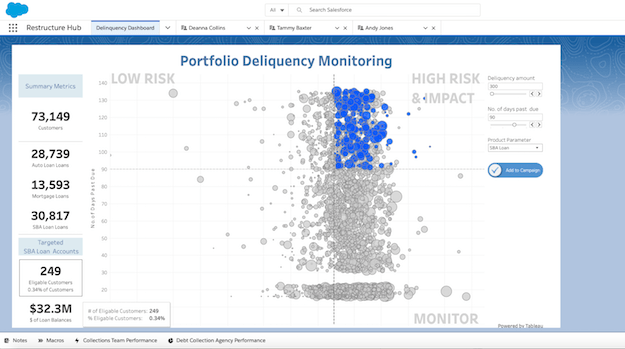

Use your analytics and insights as a north star to identify the areas to automate workflows and action plans. Below is an example dashboard indicating small business loan customers as an emerging category of risk.

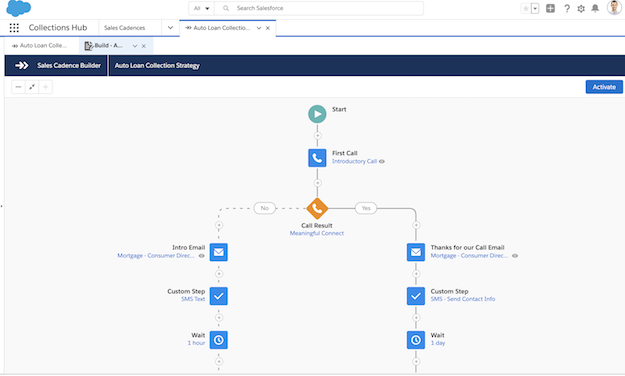

While some government programs may phase out over time, you’ll need an agile foundation to continue to help customers. You can create your own programs for financial health checks, loan recovery, and debt collections. Having an agile platform will help reduce costs while increasing efficiency across all channels to support remediation, risk, hardship, and expeditious responses.

As customers are inundated with news updates, there is an ever-pressing need to be transparent and compassionate. To get ahead of expectations, create proactive communications, to educate customers on how the evolving world affects their financial wellbeing.

Based on a customer profile, initial communications should be segmented on their preferences and put in an awareness campaign journey. You can set a defined series of activities based on how a customer is interacting with emails, employees, and other content.

A mobile app or a portal are channels you can personalize to unique customer needs. With customer data, you can tailor the digital experience with relevant information. If a mortgage customer, for example, recently lost their job, you would want to include resource articles on the available mortgage forgiveness programs.

Arm your employees with the training and knowledge to be compassionate. There is a massive need to train employees to inject empathy into customer conversations. According to the Consumer Financial Protection Bureau, 27% of complaints are related to debt collections, making it the top subject of complaints. A collections agent needs to have the ability to understand a customer's financial position, how they may be feeling, and what options they have.

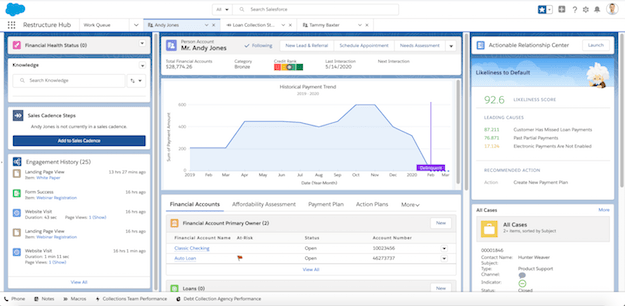

The above provides a 360-degree view of the customer in Financial Services Cloud that shows financial accounts, relationship map, documentation, financial health, and engagement history. Data powered intelligence can provide customer insights such as likeliness to default and recommend next best actions for assistance plans. To improve employee collaboration and productivity, you can automate task sequences for plans, including for a COVID-19 financial well-being plan. Consider collecting feedback from customers to drive new solution development, process improvement, and audit requirements.

In 2008, banks and lenders were at the center of the recession, ultimately harming customer trust and loyalty. Today, there is an opportunity to evolve to a new business model that puts customers at the center of your decisions while stabilizing your risk exposure. This requires banks to embrace being uncomfortable with balancing a new normal and compassion. Those who rise above reactive strategies and focus on proactively being there for customers in the midst of any crisis will prevail as a social leader, becoming the bridge to economic recovery.

We know the future is uncertain, and we are here to help. Learn more about how to alleviate financial stress for families and businesses by viewing our webinar. Become the bank your customers trust.