Get your FREE 30-day trial.

Start by selecting a product:

Salesforce ANZ’s Shreya Sethi believes this is particularly true for the local market. In an inflation-driven economy that faces lingering impacts from the pandemic, consumers have become used to digital-first experiences and expect to see this in every aspect of daily life. As Senior Director and Head of Financial Services for Business Value Services, Shreya has seen banks, insurers and wealth advisers being forced to rethink customer journeys as digital-first to meet the market.

“That's the customer's first expectation: ‘I want to be able to access things easily and through the channel of my choice.’ Mortgage lending startup Athena is one such successful startup — offering a swift, 15-minute application process. It is easy, intuitive and has competitive rates. As a consumer, why would I choose to go through a cumbersome, paper-based process with another provider when options like this are available?”

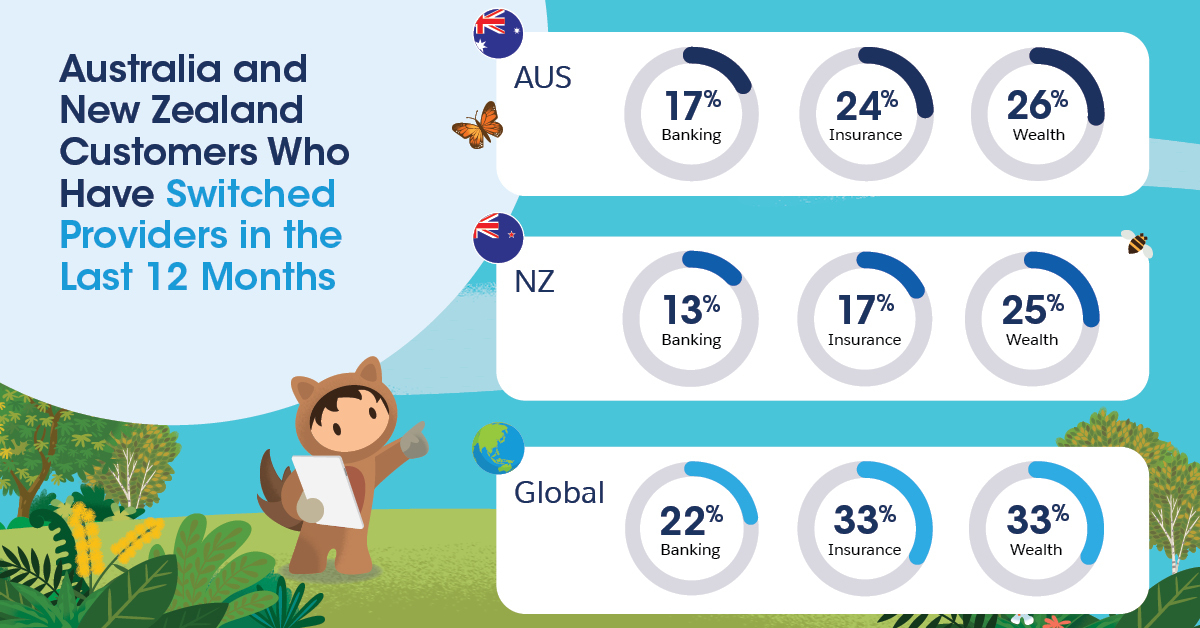

This focus on delivering better digital experiences is also a retention and survival move. As local interest rates and costs of living rise, the report shows consumers are more willing to shop around for better alternatives that meet their needs. Global customer churn rates are substantial at 22% for banking, 33% for insurance and 33% for wealth.

Future of Financial Services Report: Australia and New Zealand customers who have switched providers in the last 12 months

Although A/NZ fares better than global averages, churn is nevertheless high and can be partially explained from the reasons for switching providers.

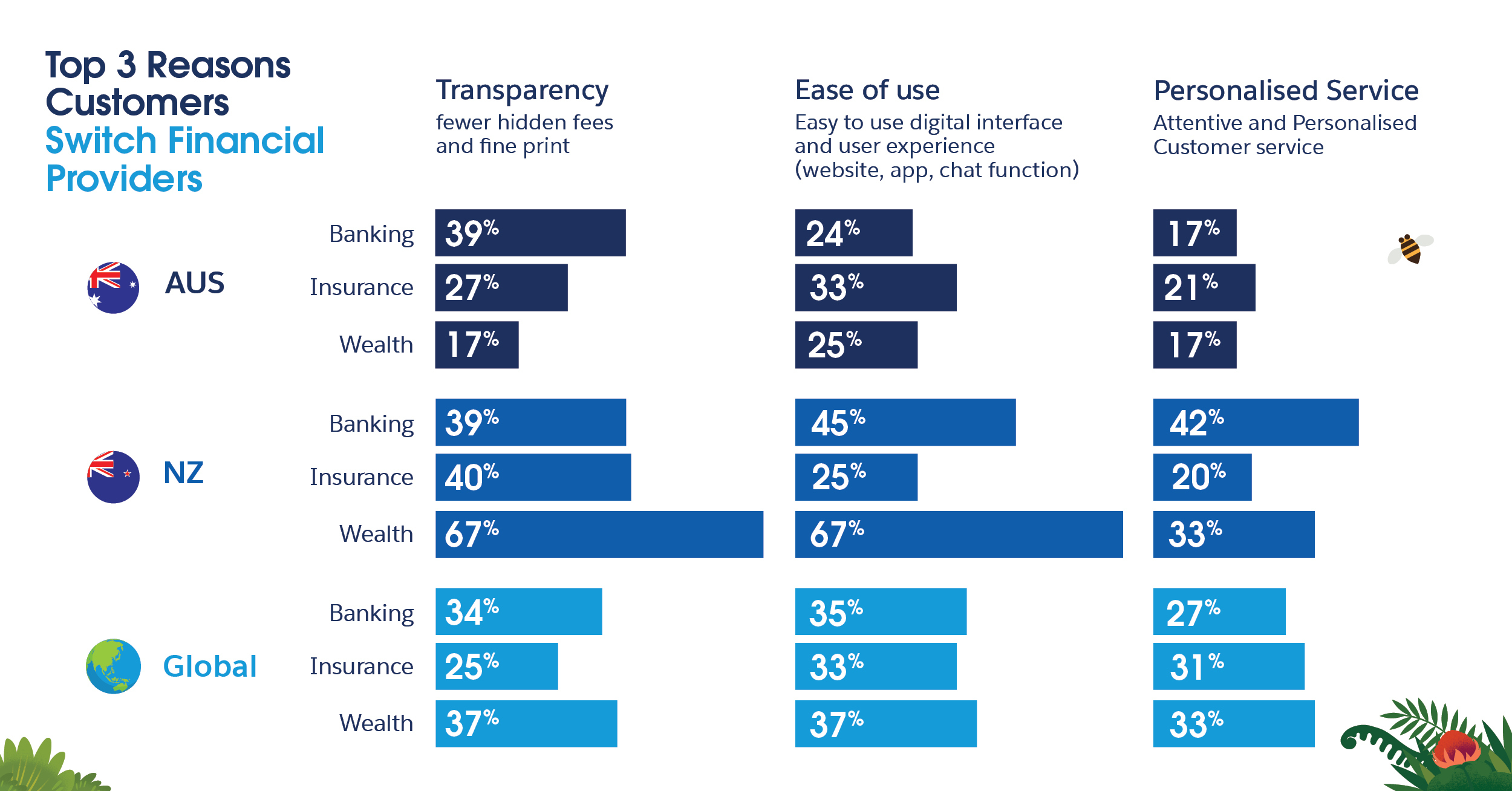

A common trend is the lack of trust A/NZ customers have in their local providers. The biggest driver for switching providers was ‘hidden fees and fine print’ (39% across A/NZ).

When it came to data privacy concerns, A/NZ fell mostly behind global benchmarks. Shreya attributes this high bar for transparency standards to the Royal Commission findings, alongside less than transparent communication by traditional providers.

“Before the pandemic, financial services operated in a very different market,” Shreya says. “I think we were more tolerant of average service and more of us accepted poor digital journeys. I don't think that's going to fly now, especially since a lot of the fintechs and D2C brands are nailing this in the market.”

The report highlights three key trends in the future of financial services. To retain and delight customers in a post-pandemic economy, successful providers of the next decade will need to excel in the following areas.

Shreya says this market expectation for seamless online experiences is also driven by emerging financial technology firms (FinTechs) with digital-first services that are raising the standard across the financial services industry. You only need to look at Nano Digital Home Loans which can provide digital end-to-end unconditional loan approvals in a matter of minutes.

“With more FinTech innovation happening in Australia, the banks will also have to evolve and innovate at the same pace so as not to lose customers.”

The report also reflects this consumer trend towards FinTechs for their simplicity. When asked why they didn’t use a traditional provider, A/NZ customers highlighted ‘easy and fast setup, verification, onboarding, and first time use of the app’ and ‘easy and intuitive user interface/user experience and navigation of the app’. Percentages for both were above global averages.

Future of Financial Services Report:Why Australian and New Zealand customers are trying non-traditional FSIs.

To truly improve on seamless experiences, providers need to lift the hood on how they operate behind the scenes. The global average for seamless customer experiences after being transferred to a customer service agent or service channel is poor — a maximum of 19%. This number is even lower in Australia and New Zealand, a maximum of 15% and 12%, respectively.

Shreya believes this disjointed service experience comes from the number of applications and manual processes being used.

“If you look at a typical relationship manager or a banker, they will most likely be looking at five to seven different systems and screens per day (and no doubt some scribbly notes on paper). The employee experience is manual and disjointed which leads to poor service & customer experience. Processes are far from being automated or connected into a single 360 customer view.“

“Efficiency and productivity is critical as we get through the slow growth high-inflation phase of the economy. It is critical to rightsize and automate the manual, repetitive tasks to free up skilled resources for complex tasks — like building customer relationships. If your digital platform can boost NPS by 20%, or improve cost-to-income ratios by enhancing productivity by 30%, you’re starting to future-proof the business. You’re setting up for the next wave of growth and innovation.”

From online searches to advertisements to Netflix choices, consumers are being delivered personalised experiences across industries like never before.

Non-curated experiences are making providers stand out — in a bad way to A/NZ customers. ‘Attentive and personalised customer service’ was the next highest driver for switching providers (17% AU, 42% NZ).

This is something that the established banks are still trying to figure out, with many still hampered by common issues associated with legacy systems: data silos across the business, no centralised source of truth and migrating on-premises data into the cloud. All of these issues make the creation of a 360-degree customer view extremely difficult.

“If I talk about my own experience as a consumer of the industry, my super and insurance providers dont understand my needs deeply. To some extent my bank does. However, any fintech I engage with, from Nano to Afterpay, instantly delivers personalised communication along with simple and easy digital processes.”

Needless to say, the reasons behind a lack of personalisation doesn’t really matter to consumers. When asked ‘does your provider anticipate your financial needs?’ only a maximum of 21% of A/NZ customers say they agree.

Delivering relevant and personalised experiences first requires your customer data to be readily accessible and easily managed. For those established providers that are struggling to digitally transform, Shreya advises taking a two-speed approach.

“Many finservs we partner with are following a two-speed transformation model, because it can take time to fix data records. We often talk about stitching the most important data sources together, then integrating them into an engagement layer which can instantly democratise personalised insights to employees and drive exceptional customer experience. The two-speed model allows organisations to start getting value and insights from data on day one, rather than trying to get to a perfect outcome on getting all their data together.”

A key theme of the global report is a continued lack of trust in their financial providers. For the A/NZ market this is particularly clear, with less than 20% agreeing with the statement ‘I trust that my provider is invested in my financial well being.’

Shreya says finding ways to build trust is a key area for future success as industry transparency and shared market knowledge continues to expand.

“There's far more transparency now [regarding] bad customer experiences and customer complaints on industry performance. Customer awareness on provider options has increased and many are now shopping around for best experience and best value. That wasn't the case four years ago.”

Customers want providers to care more about their financial well being and the insights from the report outline some key areas for improvement. To start, financial providers can regularly highlight how they protect and use customer data, remain compliant to industry regulations and make terms and conditions easily understandable.

Looking for more insights? Get the report to learn more.